Yesterday, U.S. President Donald Trump made his ‘big announcement’ on tax cuts. Some Irish eyes aren’t smiling at the prospect of the headline-grabbing reduction in the corporation tax rate from 35% to 15% actually coming to pass. Essentially, though, this latest announcement amounts to little more than reheated campaign promises, washed down with Trump’s now-familiar saccharine bombast.

This was not a well-thought out exercise in policy innovation, but rather a cheap PR stunt designed to boost his flagging ratings and attract plaudits ahead of the media-constructed – but substantially meaningless – landmark of his Presidency’s first 100 days, which falls this Saturday.

*** This article was first published on thejournal.ie on 27 April, 2017 ***

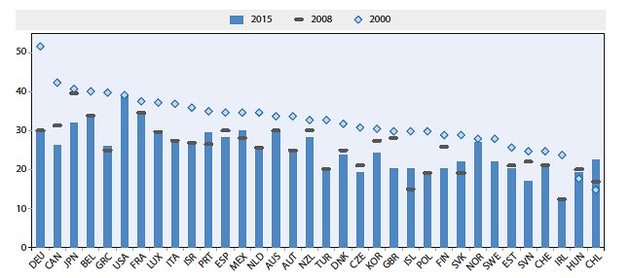

OECD Corporation Tax Rates since 2000

Source: Tax Policy Reforms in the OECD 2016

While the U.S. President may be the most powerful man in the world, passing a budget and designing tax policy is the constitutional preserve of the Houses of Congress. Of course, that doesn’t stop him – or his predecessors – from using the Presidency as a bully pulpit to try to get what he wants. As we see from ongoing attempts to repeal and replace the Affordable Care Act – a.k.a. Obamacare – there’s no guarantee Congress can deliver. And, even if they can, the final deal is likely to look very different to yesterday’s wish-list.

Changes have been made to the labyrinthine U.S. tax code over the years, but the last fundamental reforms came under Ronald Regan. Together, the Economic Recovery Act of 1981 and the Tax Reform Act of 1986 slashed the higher rate of tax from 70% to 28%, as well as making a raft of other changes. Hardcore Republicans have dreamt about going further ever since.

With a Federal rate of 35% since 1993, plus state-level taxes ranging up to 3.9%, the U.S has one of the highest headline corporate tax rates in the world. This compares to an average of 25% across the 35-member OECD. Moreover, the trend in headline rates has been downward, and accelerating, with Ireland having been in the vanguard in this ‘race to the bottom’.

Of course, that’s not the full story. In the absence of fundamental reforms – and in the presence of special interest lobbying – the American tax system has become riddled with loopholes and tax breaks. In fact, the average tax rate paid by the biggest – Fortune 500 – firms was less than 20% between 2008 and 2012.

In a fine example of American exceptionalism, they do things a little different to most countries. Up to now, U.S. citizens and companies are obliged to pay U.S. taxes on their worldwide income, no matter where they live or are incorporated. In practice, the existence of so-called ‘double taxation treaties’ with other countries, means that only this only applies where the relevant individual or corporate tax rate is lower in the other country than in the U.S.

Often, for U.S. citizens, this isn’t a big issue, since U.S. tax rates on individuals are already quite low, and about to get lower, so they don’t have to pay anything to the I.R.S. (the U.S. equivalent of our Revenue Commissioners) back home. For firms, however, the tax differential can be enormous. Apple Inc. paid an average rate of only 0.005% in Ireland in 2014, on its European profits for example. In theory, the balance – adding up to the Federal rate of 35% – is owed to the I.R.S.

But, here’s the rub… this tax is only payable upon repatriation of profits to the U.S. And, repatriation can be deferred indefinitely. This is why many of the biggest American firms maintain mountains of cash overseas. The Fortune 500 held an estimated USD 2.5 trillion ($2,500,000,000,000) overseas in 2015 – two thirds of which is accounted for by the 30 biggest, and 8.6% by Apple Inc. alone – and add about USD 100 billion to this pile every year. But, these cash piles can only be returned to shareholders in the form of dividends when repatriated to the U.S. Basically, they have been playing a giant game of chicken, waiting for the U.S. government to sweeten the deal before bringing home the bacon.

So, how do Trump’s latest tax proposals fit in, and what would they mean for Ireland?

Any decrease in the U.S. corporation tax rate makes Ireland relatively less attractive as an FDI destination for tax reasons. A headline rate of 15% – if it were to be achieved, which is in any case unlikely – could be a game-changer.

Any significant reduction in the headline rate will see a slowdown – and possibly a reversal – in the trend in so-called ‘re-domiciliations for tax purposes’ whereby vast swathes of intellectual property are transferred, for example, from Silicon Valley to Dublin’s Silicon Docks. That would be the end of Leprechaun economics! Similarly, any one-time amnesty or reduced rate offered on the repatriation of profits is likely to have the desired effect – a Westward flood of cash across the Atlantic.

But, while the amount of profit, tax, cash and intangible assets involved could be astronomical, hurting Irish tax revenues and growth figures, it doesn’t necessarily follow that significant numbers of jobs will be lost, or that real living standards will be reduced. It certainly doesn’t mean all U.S. multinationals will up and leave at once, just that any part of their operations located here – or in Luxembourg, the Netherlands etc. – solely for tax reasons is vulnerable to relocation back to the U.S. Of course, they will still need a European base for their manufacturing and sales operations, but the IDA’s trifecta of ‘tax, tech and talent’ may find itself short a ‘T’.

In a sense, we can’t say we weren’t warned. John Kerry, in 2004, and Barack Obama, in 2008, also campaigned for the U.S. Presidency on pledges to reform the corporate tax code by reducing the headline rate, eliminating loopholes, and encouraging the repatriation of profits. More recently, both the OECD and the EU Commission have been working (separately) to harmonise the rules of the game relating to the corporate tax base – what is taxed and where.

On the plus side, Ireland – and any country relying on international trade – can be relived that the Trump administration appears to have ditched support for the ‘border adjustment tax’ that had been under consideration by Congress for months. This could have had a similar impact to a tariff, and been detrimental to Ireland’s economic model.

Maybe a pertinent question for Ireland’s policymakers and commentariat is whether it is sustainable or justifiable any longer for such a large and growing proportion of our tax revenues to be so dependent not on our own tax system, but on the one designed in Washington D.C. In the medium-term, thought will need to be given to further broadening Ireland’s tax base to sustain investment in improved infrastructure and public services – critical components of any enlightened offering by Ireland Inc. to potential FDI investors.