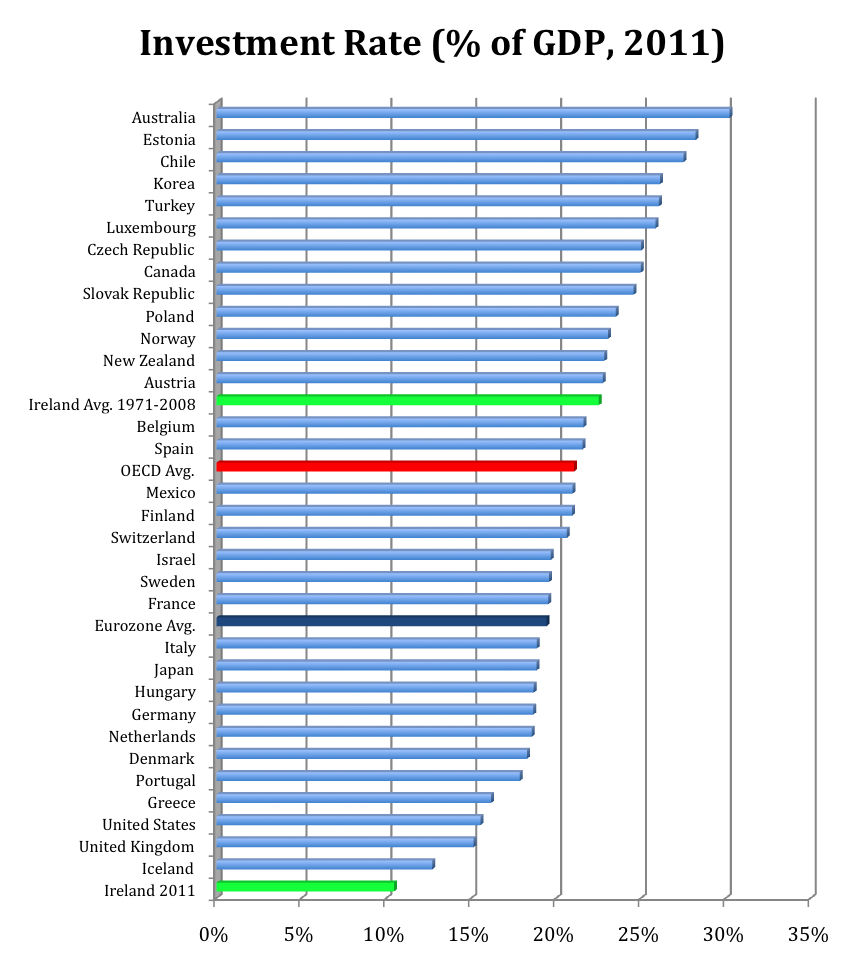

At 10%, the Irish investment rate (Gross Fixed Capital Formation / GDP) in 2011 was less than half the OECD average in 2011, half the Eurozone average, only four fifths that of Iceland, the next lowest OECD member at 12.7%, and less than Greece (16.2%), Portugal (17.9%), Italy (18.9%) and Spain (21.6%).

In a previous post, described the changing composition of Irish GDP and noted the rise and fall of the ‘Investment’ component. Ireland’s overall investment rate, which averaged 22% of GDP over the 1971-2008 period, has fallen to a low of circa 10% in 2011 and 2012. Even in the 1980s, by comparison, the investment rate averaged 22.5% and never fell below 18.6%.

Essentially, economic growth is derived from three sources: 1) capital accumulation through investment, 2) an increase in the labour force, and 3) and improved productivity, i.e. the process through which the factors of production are converted into output. Investment can support productivity growth, and is required in sufficient amounts at least to keep pace with depreciation and labour force growth if capital intensity is to be maintained.

At the firm level, investment in plant and machinery increases its future productive capacity. At an economy-wide level, investment in infrastructure not only benefits citizens directly but increases the productive capacity of the economy as a whole. With record low investment rates, Ireland is in danger of undermining its capacity to generate jobs and growth both now and in the future.